When to Consider Life Insurance for a Child: Key Milestones

When it comes to buying life insurance for a child, we promise – it’s not what you think.

Rather than planning for their death, life insurance is about preparing for your children’s future – their financial future. Just like you might invest in a child’s RESP, whole life insurance for kids comes with an investment component that can grow over their lifetime.

The best part? This investment grows into money they can access when they really need it – whether to complement an RESP and fund their post-secondary education, help pay for a wedding, or be put towards a down payment on their first home.

Not to mention, getting life insurance for a child while they’re still young and healthy is the most affordable time to buy – and it means they have guaranteed coverage later in life – you know, when they’ll actually need it.

Of course, it’s always important to do your research and compare your options so that you can be sure you’re purchasing the best life insurance for your child’s future.

When to consider life insurance for a child

With every milestone comes a new opportunity to consider life insurance – but remember the earlier you buy, the lower the cost will be. Below are reasons to consider life insurance at different stages of a child’s life.

Birth or Early Childhood (Ages 0-5)

Why now? As long as your child is healthy, the cost of coverage will never be more affordable than now. And, because price goes up with age, you can lock in low premiums (i.e., the amount you pay for an insurance policy) that will never go up.

Benefits: Whole life insurance for kids, especially if started in early childhood, has the maximum amount of time to build on that investment (called the cash value¹) and accumulate savings.

Birth or Early Childhood

Whole life insurance for kids, especially if started in early childhood, has the maximum amount of time to build on the cash value and accumulate significant savings.

Starting School (Ages 6-12)

Why now? The whirlwind of the early years have come and gone. Now that things have started to slow down a little, parents have more time and energy to think about securing their children’s future financial needs. Investments, like an RESP or whole life policy for kids, where the cash value may be used later become top of mind.

Benefits: There’s still time to lock in those affordable premiums. Plus, grandparents may be interested in gifting coverage at this stage of life – especially for kids who “have it all.”

Starting school

There’s still time to lock in those affordable premiums. Grandparents may be interested in gifting coverage at this stage of life – especially for kids who “have it all.”

Teen Years (Ages 13-17)

Why now? Your child may be getting their first job or thinking about the cost of their post-secondary education. That’s why now is a practical time to discuss financial responsibility and introduce them to concepts like savings and insurance.

Benefits: Securing a policy before adulthood, especially if there’s a family history of health conditions, ensures your child is covered for life – despite any health diagnoses at a later stage. Not to mention, they still have time to grow the cash value, which could be tapped into for significant life expenses like a wedding or a first home.

Teen years

Coverage may support future family and financial goals, and the cash value can be used as an emergency fund, to help fund expenses that come up later in life, or could provide income during retirement.

Approaching Adulthood (Ages 18-21)

Why now? Life insurance policies taken out during this time provide financial stability as the child transitions into adulthood and gains financial independence. At this stage, they may have student loans or other debt that would need to be paid off if something were to happen to them.

Benefits: Coverage may support future family and financial goals, and the cash value can be used to help fund expenses that come up later in life or even retirement.

Approaching Adulthood

Securing a policy before adulthood ensures your child is covered for life – despite any health diagnoses later. And they still have time to grow the cash value, which could be tapped into for significant life expenses, like a wedding or a first home.

Common reasons for buying child whole life insurance

We’ve said it before and we’ll say it again: Child life insurance truly has nothing to do with a child’s death and everything to do with planning for their long, healthy life. Below, you’ll find the two most common reasons for purchasing whole life insurance for a child.

1. Building Cash Value for Future Needs

Whole life policies for kids have an investment portion, called the “cash value,” which can accumulate nicely over time. This is money they can use later in life for big expenses, as an emergency fund, or as income during retirement.

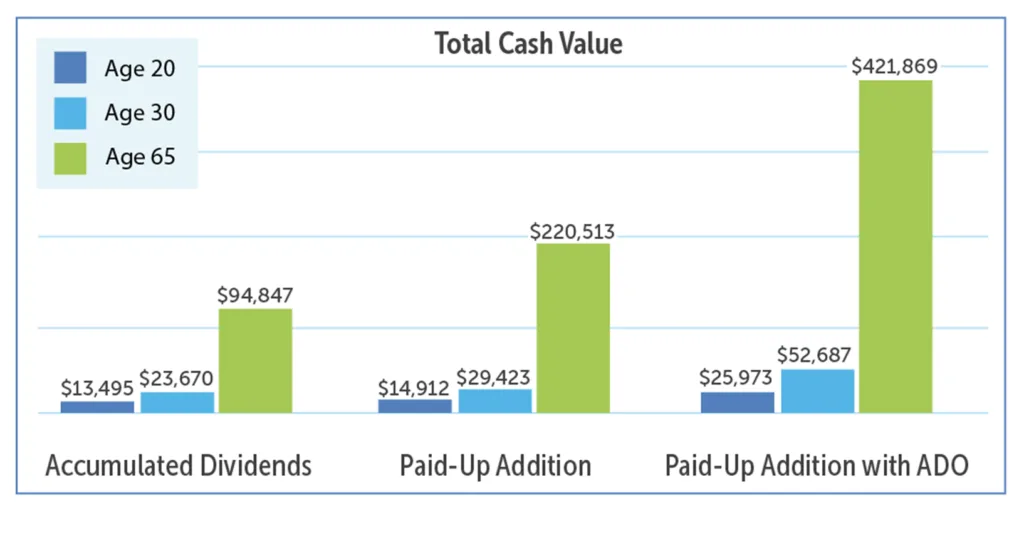

Parents who are looking for the highest growth potential should speak to their advisor about taking advantage of the no-cost Paid-Up Addition (PUA) feature as well as purchasing the Additional Deposit Option (ADO) on top of that.

While purchasing ADO will cost a little more each month, in this scenario, the policy would be earning interest on its interest – compounding the growth in ways that will impact your child’s financial future in a much more significant way.

How Additional Deposit Option Can More Than Double a Policy’s Growth2

2. Securing Future Insurability

Families with health history concerns may choose to purchase life insurance for their child to guarantee future insurability. But keep in mind that guaranteed insurability is a major pro for even the healthiest of families. Because as we age, most of us will be diagnosed with age-related health conditions – which can make life insurance unaffordable for everyday Canadians. If you’d like to make sure your child has affordable life insurance in place when they’re an adult, there’s no better time than the present.

Typical coverage amounts for children

When it comes to child life insurance, most providers in Canada offer coverage ranging from $10,000 to $50,000, though higher coverage amounts are available with some carriers.

Many families find that policies in the $25,000 to $50,000 range provide a balance of affordability and future cash value benefits. Even better, parents who opt for 20-pay whole life insurance know there’s an end in sight when it comes to making payments. That’s right, payments stop after 20 years – yet their child remains covered for life.

Key factors to research when choosing a policy

Choosing the right insurance policy can feel overwhelming, especially with so many options and fine print to sort through. But making an informed decision is crucial — it’s not just about finding a policy that fits your budget, but one that truly meets your needs and protects what matters most. In this section, we’ll break down five key factors you should research before selecting a policy, helping you navigate the process with confidence and clarity.

1. Cost and Affordability

It’s always a good idea to compare costs, but keep in mind that some insurers provide a little extra, like member benefits or support for beneficiaries. While child life insurance is extremely affordable, higher coverage generally means higher cost. Be sure to aim for an amount that fits comfortably within your budget.

2. Additional Features

Consider additional optional benefits (also known as “riders”), like Guaranteed Insurability Option or Owner Waiver and Disability Benefit. You can select these riders at the time of purchase to further customize your child’s policy. And as mentioned earlier, features like the Additional Deposit Option (ADO) can result in a much larger potential for growth.

3. Potential for Growth

Research how different policies accumulate dividends3 as well as how the projected rate of return over time can impact total cash values.

4. Insurance Provider’s Reputation

Choose a financially stable insurer with strong customer reviews and a solid reputation for paying out claims.

5. Other Investment & Savings Options

Consider other options, like an RESP or savings accounts, that may offer different benefits or growth potential. Even better, create a holistic financial plan that includes all of the above. Complementing an RESP with whole life insurance for a child is never a bad idea!

Potential drawbacks of children’s whole life insurance

Life insurance for a child is indeed a smart move for many — after all, who doesn’t want to give their child a financial head start? But it’s important to take a step back and look at the full picture. Like any financial product, it has its pros and cons. Below are some potential drawbacks to consider as you decide whether or not whole life insurance for kids truly fits your goals.

Opportunity Cost of Investment

If you don’t opt for the ADO, other investment or savings options may potentially yield higher returns. That said, life insurance for a child can pair well with traditional RRSPs and the potential for growth can be significant when you let compound interest do its thing.

Surrender3 Charges and Fees

If, for any reason, you need to cancel your child’s policy, this decision could result in a reduced cash value or possible surrender fees. Ask your advisor to go over this with you so you have a full understanding before you commit.

Limited Flexibility

Regular whole life policies are a long-term commitment, which may not suit all families. Of course, 20-pay whole life can be a great option for parents who’d like payments to eventually stop while ensuring their child has coverage for life.

Questions to ask before buying life insurance for a child

Buying life insurance for a child isn’t a one-size-fits-all decision — it really depends on your financial goals, your family’s needs, and how you view your long-term planning. Below are some questions you may want to ask your advisor before making a final decision.

- Can you help me weigh the long-term costs vs. benefits of this policy?

- How does the cash value grow, and when can my child access it?

- Are there any restrictions when it comes to accessing the cash value?

- What riders, features, or benefits are available?

- What happens if payments are missed?

Should you buy whole life insurance for your child or grandchild?

It’s a big question — one that doesn’t always come with a simple yes or no. Whole life insurance for a child or grandchild can be appealing for a few reasons. On the plus side, it locks in low premiums for life, builds cash value over time, and can offer a sense of financial security. For some families, it’s also seen as a thoughtful, long-term gift.

But remember: In order to see a meaningful return, you may need to take advantage of compound interest via ADO – and this will add to the cost.

In the end, it really comes down to your family’s goals. Ask yourself: What are you hoping to achieve in the long run? Where does a whole life policy for your child fit into your overall financial plan? If you’re unsure, it’s always a good idea to speak with a financial advisor who can help you weigh the pros and cons based on your unique situation.

Why choose Serenia Life for child life insurance?

As a member-based organization whose roots go back nearly 100 years, we encourage kindness by sharing our profits through community outreach, fundraising, and unique member benefits that help Canadians support their family, their community, and the causes they care about. The more we grow, the more we can give.

We provide members with access to a growing collection of member benefits that make a positive impact on their lives and the lives of others. Benefits, such as:

- $2,500 post-secondary scholarships

- Up to $600 towards fundraising events, and up to $400 to cover volunteering expenses in Canada

- Financial support for legal wills through a lawyer

- And much more!

View a full list of our member benefits.

The bottom line

Whole life insurance for a child isn’t just a policy — it’s a long-term gesture of love and protection. For some families, it can be a quiet but powerful way to plant seeds for their child’s future, offering both financial security and peace of mind that grows over time. It won’t be the right choice for everyone, and that’s okay. What matters most is making a decision that reflects your family’s values, goals, and the kind of future you want to help create for your child or grandchild. Ready to take that first step? Book a no-obligation call with one of our licensed advisors today!

Disclaimers

¹Cash values are accessible via a withdrawal, policy loan, or surrender. These may be subject to taxation and a tax slip may be issued. Accessing the policy’s cash value will reduce the available cash surrender value and death benefit.

²Illustration only, as of November 2025. Age 0, male regular rates with $50,000 insurance coverage and using current dividend scale. Future performance will be different than illustrated due to the variability of the dividends. Dividend options used are Accumulated Dividends, Paid-up Additions and Paid-up Additions with Additional Deposit Option of $27.08 per month. All numbers in CDN $. The policy is “paid up” at Age 20

3Dividends are not guaranteed and are paid based on the overall experience of Serenia Life Financial, considering all the risk factors. Dividends may be subject to taxation. Dividends will vary based on the actual investment returns in the participating account as well as mortality, expenses, taxes, lapses, withdrawals, and other experience of the participating block of policies. They have the potential to increase the value of your policy above the guaranteed amount, depending on the dividend option selected.

4Policy surrender can either be partial or full surrender of the cash value of the policy. A partial surrender will reduce the value of the policy. A full surrender means cancelling the policy and receiving the cash value less any surrender fees. Beneficiaries won’t receive any death benefit upon full surrender. There may be tax on the amount received that is above the adjusted cost basis.

{kind=link}

{kind=link}

{kind=link}

{kind=link}