A Guide to Life Insurance for Kids in Canada

Parents who are able to lay an early foundation for their children’s financial security often buy whole life insurance with an investment component as early as possible. Here’s what you need to know about the advantages of including your children in your family’s financial plan.

Let us help you find

the right insurance

Why do kids need life insurance?

Most kids probably don’t need life insurance because they don’t earn a living and they don’t have any assets to protect. But, as every parent knows, kids grow up fast and they become adults who will need and likely want life insurance coverage when they get older and start their own families.

When you buy a policy for your children or grandchildren, you’re thinking about their future by making it much easier for them to maintain coverage for life. This may not seem like a top priority now, but becomes very important once your child grows up and has a family of their own – even more so if the child develops a medical condition that could either make it unaffordable or impossible to get coverage later.

Another really important reason to buy life insurance for your kids or grandkids is that it acts like an investment that grows over the course of their long lives – this is money they can access when they really need it. They won’t think this is important because kids don’t tend to plan that far ahead. However, you’ll have the peace of mind that comes with knowing you’re doing the planning for them.

Learn more about investing in your children’s future with life insurance.

Debunking common myths about life insurance for kids

Myth #1. Children don’t earn money so they don’t need life insurance.

Adults need life insurance to replace any income they would have earned before their retirement. This leads some parents to believe that kids don’t need insurance because they don’t earn a salary. While it’s true the kids aren’t bringing home a paycheque, the benefits of insuring your child include protecting what matters most and ensuring your child has a financial leg-up.

Myth #2. Life insurance is expensive.

The opposite is true when it comes to babies and children. Life insurance is extremely affordable when a child is young and healthy. You’re also locking in low-cost coverage now, guaranteeing the same price later in life, despite health conditions that might develop in adulthood.

Myth #3. Buying life insurance means I think my kid is going to die.

In fact, it means you think they’re going to live a nice, long life. You wouldn’t invest in their future otherwise. Remember, in most cases, you can only buy permanent life insurance for kids – and that means you’re safely going to live a nice, long life. In fact, it’s recommended not to buy term life insurance for children in Canada because we all plan for our little ones to live well beyond a term of 10, 20, or 30 years!

Myth #4. Life insurance means I would benefit from my child’s death.

Every parent knows the real benefit of children is watching them grow and turn into amazing adults with meaningful lives of their own. The amount of life insurance coverage that a typical parent would purchase is not life-changing money, it’s just enough to pay for the expenses that may arise in this very unlikely scenario.

Myth #5. Life insurance is a poor investment.

Permanent insurance comes with a cash value1 portion that typically includes lower-risk investments for earning and preserving wealth over a child’s lifetime. The return on investment will be similar to any other low-risk investment over time. And keep in mind, the cash portion in your child’s policy grows tax free – not to mention, the death benefit is also tax free when it’s paid out eventually. Pro tip: If you have extra money to invest, consider putting it towards a feature called Additional Deposit Option2, which can lead to exponential growth. Learn more

A word on risk

A word on risk: If you want to place some of your money in higher risk investments to take advantage of a higher earning potential, do it in other parts of your financial plan to offset the more conservative nature of the growth in a permanent life insurance policy. Talk to your advisor about the role of diversification in financial planning.

Myth #6. If I’m paying into an RESP for my child, that means I don’t need to invest in life insurance.

An RESP is a great first step when it comes to planning for your child’s financial future. But keep in mind, it’s savings for your child’s post-secondary education only. The growth in a life insurance policy can be used for any purpose – from paying for a wedding, to helping cover a down payment on a home, to using it to fund their retirement one day, the possibilities are endless.

How much can my child’s policy grow over time?

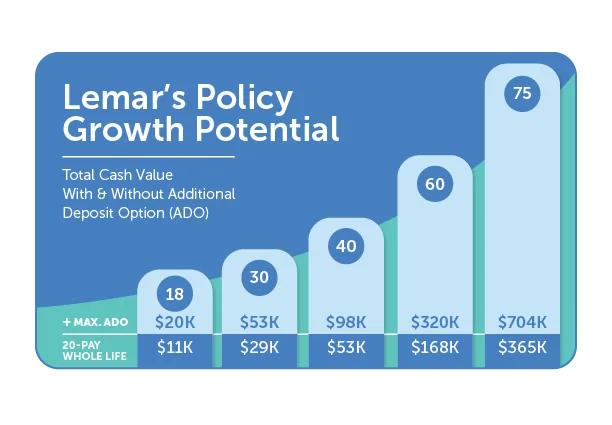

Scenario 1: Susan and Lemar

Scenario 1: Susan and Lemar

Budget: $90 / month (but she’d like to spend less, if possible)

Primary goal: Invest in my child’s future

Secondary goal: An end in sight when it comes to payments

Susan’s goal was to set up her six-month-old son Lemar for greater financial stability decades from now. To make the most of her $90-a-month budget, a Serenia Life advisor presented her with two options: a 20-pay whole life insurance policy with a $50,000 payout and an investment component with or without the Additional Deposit Option (ADO) feature.

Option 1

Basic 20-Pay Whole Life Coverage

Monthly Cost: $57.15

Option 2

Basic 20-Pay Whole Life Coverage +

Max. Additional Deposit Option (ADO)

Monthly Cost: $84.23

With a 20-Pay Whole Life Policy, Susan can rest easy knowing payments will stop after 20 years – but Lemar’s coverage will stay in place for the rest of his life. Without her advisor’s expert guidance, Susan wouldn’t have known that she could double Lemar’s growth and still remain under budget.

Growth Potential Over Lemar’s Lifetime (Option 1 vs. Option 2)

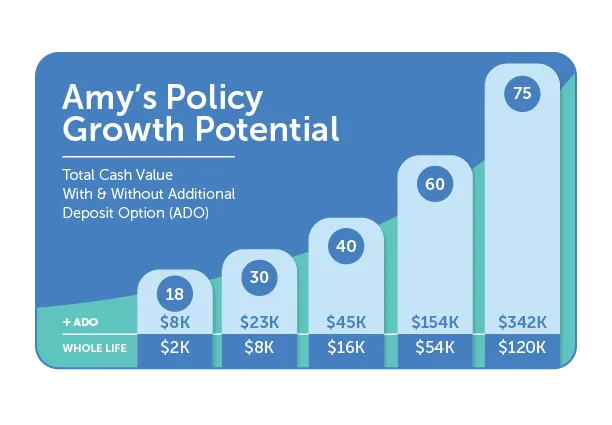

Scenario 2: Sergio and Amy

Scenario 2: Sergio and Amy

Budget: $35 / month

Primary goal: Invest in my child’s future

Secondary goal: The most affordable option

Sergio doesn’t have a lot of extra income to spend, but it’s important to him that he set up his one-year-old daughter, Amy, up for the future. Keeping his monthly budget of $35 in mind, a Serenia Life advisor presented him with two options: a whole life insurance policy with a $25,000 payout and an investment component with or without the Additional Deposit Option (ADO) feature.

Option 1

Basic Whole Life Coverage

Monthly Cost: $20.03

Option 2

Basic Whole Life Coverage +

Additional Deposit Option (ADO)

Monthly Cost: $38.36

With a whole life policy, Sergio will be getting the lowest possible price – but he will have to pay for the rest of Amy’s life. Sergio understands that when Amy is grown and making money of her own, he can transfer ownership of the policy to her, and she can take on the payments, giving him some financial relief in the future. While option 2 is over budget, Sergio’s advisor wanted to demonstrate how much more growth was possible if he just spent a few dollars more each month.

Growth Potential Over Amy’s Lifetime (Option 1 vs. Option 2)

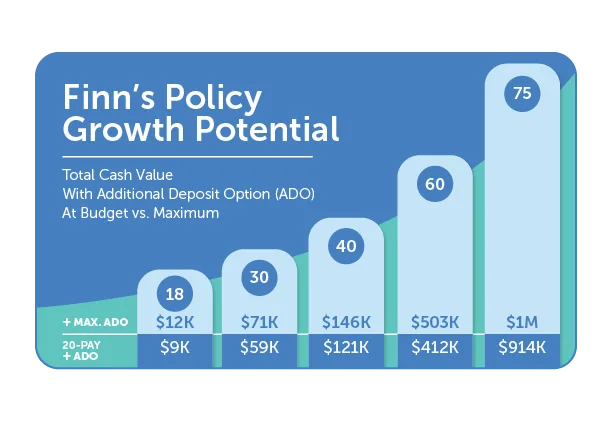

Scenario 3: Sara and Finn

Scenario 3: Sara and Finn

Budget: $175 / month

Primary goal: Invest in my grandchild’s future

Secondary goal: As much growth as possible

Sara is living a comfortable retirement and has extra money she’d like to spend on her 10-year-old grandson Finn’s future. With a monthly budget of $175, a Serenia Life advisor presented her with two options: a 20-pay whole life insurance policy with a $100,000 payout and an investment component with Additional Deposit Option (ADO) feature at budget versus the maximum she could spend.

Option 1

20-Pay Whole Life Coverage + ADO at budget

Monthly Cost: $178.70

Option 2

20-Pay Whole Life Coverage + max ADO

Monthly Cost: $207.86

With a 20-pay whole life policy, Sara doesn’t have to worry that Finn will have to take on the cost one day, and she plans to be around to pay off the entire thing. She has made clear that she wants the best investment possible for her one and only grandchild. That’s why her advisor showed her just how much more growth was possible if she chose to go with “max ADO,” which is about $30 over budget.

Growth Potential Over Finn’s Lifetime (Option 1 vs. Option 2)

What are some other benefits of life insurance for kids?

Guaranteed access to coverage and a head start on financial security are good reasons to consider purchasing whole life insurance for kids. But there are other benefits, including:

Education or other expenses

Permanent life insurance, discussed in detail below, allows the policy owner to accumulate cash in the investment component of a whole life insurance policy. Once your child is of legal age, the money can be withdrawn tax-free and used when they need it most.

Policy owner benefits

When you purchase a life insurance policy from Serenia Life, you get customized coverage plus a range of member benefits that include scholarship opportunities, financial support for charitable work, free online wills, and more.

Time to grieve and heal

In the tragic event of a child’s death, the death benefit (i.e., a payment made to designated family members, other loved ones, or the charity of choice after the insured’s death) can allow parents to take time off work to focus on the tough task of coping with their loss.

Learn about what to look for when shopping for the best life insurance in Canada.

Types of life insurance you can purchase for your kid(s)

Insurance is a critical component in a family’s overall financial plan. Many parents consider the cost of their policy an investment, rather than an expense, because it protects them from having to sell assets, like a property, to cover expenses, like a mortgage. Here are three of the most common types of insurance for kids.

Whole life insurance

Whole life insurance is a form of permanent coverage that never expires as long as you continue to make the payments. Along the way, a portion of your monthly or annual premiums (i.e., the amount you pay for an insurance policy) gets invested and earns interest in the form of dividends1. This is called the cash value2 portion of your policy and it’s what your child can use in future to pay for education, a down payment on a home, or other expenses. This is why many families often “think outside the bank” and see permanent life coverage as a solid, long-term investment.

Serenia Life’s Grow With Them Plan

Our Grow With Them Plan is whole life insurance with an investment component that grows with your child. This plan can be purchased for a child as young as 14 days old, and up ‘til they hit their double digits. When you buy child life insurance, you’re setting your little ones up financially for the future. Just like you would invest in an RESP to help fund a child’s post-secondary education, the Grow With Them Plan comes with a cash value that has the potential to grow quite significantly over time. The best part? When they’re all grown up, your child or grandchild can access this money when they need it – to fund a wedding, to help with a down payment on a home, or even to help them out when they retire one day.

Serenia Life’s All Grown Up Plan

Our All Grown Up Plan is whole life insurance with an investment component for teens and pre-teens. Sure, they think they’re all grown up – but when it comes to their financial future, they still need our help. And when you buy life insurance for this age group, you’re setting them up for a future that may seem scary and unaffordable to them. 59% of young adults in Canada are concerned they may not be able to afford a home (source) – that can feel like a pretty bleak future for our teens. But, just like you invested in an RESP to help fund their post-secondary education, the All Grown Up Plan comes with a cash value that has the potential to grow quite significantly over time. The best part? Your child or grandchild can access this money to help fund a down payment on a home, emergency expenses, or even retirement.

Whole life insurance versus 20-pay whole life

For both plans, parents can choose between whole life or 20-pay whole life insurance – both are permanent forms of life insurance, but with a 20-pay policy, payments stop after 20 years.

At what age should I consider getting life insurance for my child?

“The sooner the better,” especially when it comes to putting the power of time on your side. Whether your goal is to provide your kids with guaranteed access to coverage later in life, or you want to fund an investment that will grow for decades, it pays to start early – literally – when coverage is relatively inexpensive, and their policy has years to earn interest and grow.

How do I choose the right life insurance for my kid(s)?

Like most financial decisions, searching for the right solution starts with a clear definition of what you’re trying to achieve. Here’s how to begin shopping for a life insurance policy for children, and perhaps yourself as well.

Step 1. Complete a needs assessment

Hands down, the best way to make the right decision for your family is a one-to-one chat with a knowledgeable and objective advisor.

Step 2. Research multiple providers

Research may reveal that some providers offer benefits in addition to coverage that align more with your needs and values. For example, Serenia Life offers the Bundles of Joy Benefit, a $100 baby bonus when you buy a life insurance policy for a baby in their first year.

Step 3. Get a few quotes

Life insurance for children is relatively straightforward, so don’t expect a huge variation in cost. But it still pays to shop around. You can get a free online quote on this website.

Step 4. Know what you’re buying

Purchasing life insurance from an agent allows you to ask questions and get a clear understanding of what you’re buying and how it works.

Step 5. Ask what makes each provider unique

Now, you’ve got a good idea of what life insurance will cost and narrowed down providers. To complete the process, take a look at what else they offer. For example, Serenia Life provides monthly payments for bereaved children, post-secondary scholarships, reimbursements for first aid training, a free online will, and seed money for fundraising events3. We’ll even help you pay for a lawyer to draft or update your will every five years.

Why should you choose Serenia Life for child life insurance?

As a member-based organization whose roots go back nearly 100 years, we encourage kindness by sharing our profits through community outreach, fundraising, and unique member benefits that help Canadians support their family, their community, and the causes they care about3. The more we grow, the more we can give.

We provide members with access to a growing collection of member benefits that make a positive impact on their lives and the lives of others.

Benefits, such as:

- $2,500 post-secondary scholarships

- Up to $600 towards fundraising events, and up to $400 to cover volunteering costs in Canada

- Financial support when drafting/updating a will through a lawyer

- And much more!

View a full list of our member benefits.

Let us help

Life insurance is an important part of your family’s holistic financial plan. And when it comes to your children, you’re providing them the opportunity to create lifetime wealth. To get the best long-term value for your money, talk to a licensed Serenia Life advisor. about our Grow With Them or All Grown Up Plan. They can answer any questions about the ways you can incorporate insurance planning into the things you already do to care for your loved ones.

Disclaimers

1Cash values are accessible via a withdrawal, policy loan or surrender. These may be subject to taxation and a tax slip may be issued. Accessing the cash value of the policy will reduce the available cash surrender value and death benefit.

2 Additional Deposit Option (ADO) allows you to take advantage of the tax preferred savings room within a Serenia Life Financial Whole Life policy. By choosing this option you can pay additional premiums over and above the required premium for your policy. Each of these premiums will be used to buy Paid-Up Additions, which increase the permanent protection available to you. These additional layers of coverage are combined with the Paid-Up Additions purchased with dividends to potentially accelerate your death benefit growth. Paid-Up Additions also have a cash value, which will also be increased when Paid-Up Additions are purchased with the Additional Deposit Option.

3Assuming the child is healthy

4$25,000 coverage for a 1-year-old child; payments are for life or until ownership is transferred

5Dividends are not guaranteed and are paid based on the overall experience of Serenia Life Financial, considering all the risk factors. Dividends may be subject to taxation. Dividends will vary based on the actual investment returns in the participating account as well as mortality, expenses, taxes, lapses, withdrawals, and other experience of the participating block of policies. They have the potential to increase the value of your policy above the guaranteed amount, depending on the dividend option selected.

6Serenia Life Financial’s member benefits and program are not contractual. They are subject to change and maximum funding limits.