What is Whole Life Insurance and How Does it Work?

Whole life insurance is a type of permanent life insurance that provides lifelong coverage and the ability to grow your money over time. It is a popular option for Canadians who are looking for another way to invest their money, while also protecting their family’s financial future.

Whole life insurance is a type of permanent life insurance that provides lifelong coverage and the ability to grow your money over time. It is a popular option for Canadians who are looking for another way to invest their money, while also protecting their family’s financial future.

How Does Whole Life Insurance Work?

Unlike term life insurance, which offers coverage for a specific term, whole life insurance guarantees that your beneficiaries (i.e., the person(s) you choose to receive your life insurance payment in the event of your death) receive a death benefit (i.e., a payment made to designated family members or other loved ones) at the time when you pass away, as long as the policy is active. Here’s how it works:

- You choose to make payments for your entire lifetime, or opt for 20-pay whole life, where you make slightly higher payments – but they stop after 20 years.

- You can opt to make use of the investment portion of your policy, either by borrowing from the cash value (i.e., cash that is accumulated within the policy that can be accessed at any time) or withdrawing some or all of your dividends (i.e., a portion of the insurer’s profits that are shared with the policyholder).

- In the event you choose to borrow from your cash value, you will be expected to pay it back, similar to what you would do with a loan. Except in this case, the money goes to your beneficiaries upon your death. If you do not pay it back, the amount will be subtracted from the death benefit your loved ones receive, plus any interest.

- In the event you choose to withdraw your dividends, you are not expected to pay this money back. However, these earnings will not be added to the death benefit in this case.

- Upon death, your beneficiaries are guaranteed the payout you initially signed up for – plus any earnings (assuming you haven’t used them) and minus any amount owed (assuming you borrowed from your cash value and didn’t pay it back).

Types of Whole Life Insurance

1. Traditional Whole Life Insurance

This is the most common type of whole life insurance, offering a guaranteed death benefit and fixed payments. With this policy, the death benefit and cash value accumulation are predetermined, providing stability and predictability.

2. Universal Life Insurance

Universal life insurance combines a death benefit with an investment component, but it provides more flexibility than traditional whole life insurance. Policyholders can adjust their payments and death benefit amounts within certain limits, allowing for customization to meet changing financial needs.

3. Participating Whole Life Insurance

Participating whole life insurance, also known as dividend-paying whole life insurance, offers the potential to earn dividends. These dividends are a portion of an insurer’s profits, which are distributed to policyholders. Policyholders can choose to receive dividends in cash, use them to reduce premiums, or reinvest them to increase the policy’s cash value and death benefit.

4. Limited Pay Whole Life Insurance

Limited pay whole life insurance allows policyholders to make payments for a shorter period while enjoying lifelong coverage. For example, you might choose to pay premiums for 10, 15, or 20 years, after which you no longer have to make payments. This type of policy is attractive for those who want to ensure their coverage is fully paid for by a certain age or within a specific timeframe.

Benefits of Whole Life Insurance

Coverage for life

Because coverage lasts your whole life, so too does your peace of mind. There’s no need to worry that it will run out after 10, 20, or 30 years. Plus, you can forget about the additional costs associated with renewing or purchasing a new policy at an older age, or in the event you are diagnosed with a new health condition.

The ability to grow and protect your savings

A portion of your payments goes towards building what is typically referred to as the “cash value,” a sum of money which grows tax-deferred over time. Not to mention, your dividends may continue to grow, based on market conditions. These earnings can be accessed through policy loans or withdrawals, offering a potential source of funds for emergencies, education expenses, or supplementing retirement income.

How Much Does Whole Life Insurance Cost in Canada?

The payments you make for whole life insurance are based on a variety of factors, including your age, health, gender, and lifestyle habits (e.g., are you a smoker?). The younger and healthier you are, the lower the cost will be.

With that in mind, let’s talk about investing in a child’s future, where the cost is much, much less. See the table below for a newborn (0-12 months) with different coverage amounts.

| Coverage Amount | |||||

|---|---|---|---|---|---|

| Monthly Payments | Male | ||||

| Female |

Children’s Whole Life Insurance

While it may seem unusual to consider life insurance for little ones, whole life insurance policies for children can provide a range of long-term benefits throughout their life.

The benefits of insuring your child early include:

1. Cost-Effective Payments

There is truly no cheaper time to buy than now. Compare $58 a month for a healthy 5-month-old girl versus $204 a month for a healthy, non-smoking 45-year-old woman. Both of them are looking for $100,000 of coverage.

2. Guaranteed Lifetime Coverage

Once your child is all grown up, you can transfer the policy to their name, at which point they can select their immediate family members as the beneficiaries. The amount of the death benefit is guaranteed.

3. Securing Insurability

In other words, they won’t have to worry about purchasing a more expensive policy due to their age, a new diagnosis, or a risky occupation or hobby. (Why? Because they’re already covered for life! See #2)

4. A cash value that grows with them

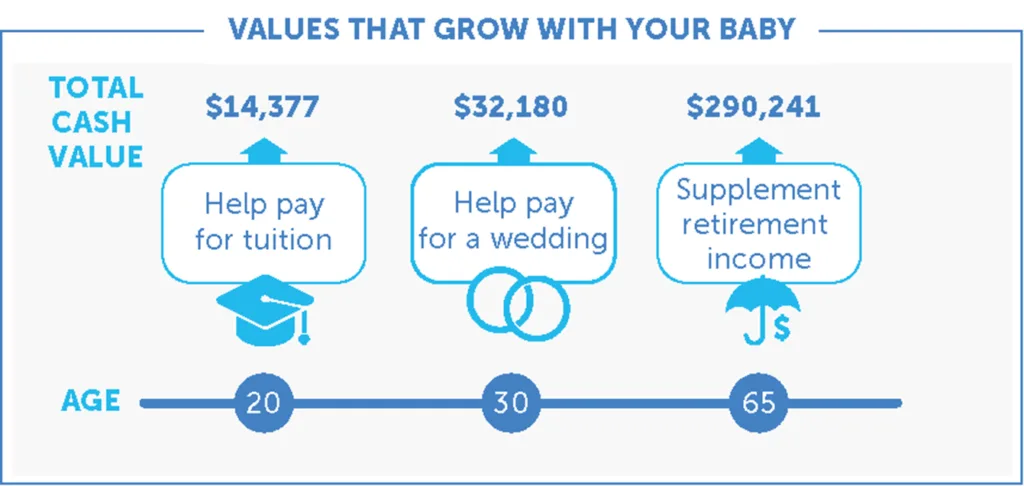

The longer your child’s policy is active, the more time the investment portion of the policy has to grow. Imagine: That 5-month old baby girl would have access to money in her policy that could be worth $14,377 by the time she is 20, $32,180 by the time she’s 30, and $290,241* by the time she is 65. These earnings could help with post-secondary tuition, a wedding, or retirement living respectively.

The numbers above are a sample illustration only, as of November 2025. Age 0 based on female regular rates, paid-up additions dividend option, and on $100,000 initial insurance coverage and current dividend scale. Future performance will be different than illustrated due to the variability of the dividend. All numbers in CDN $.

Learn more about the benefits of insuring your child

How Much Whole Life Insurance Should I Buy?

If we’re still talking about little ones, you need to think about how much money you’d like them to have access to when they’re 20, 30, or 65 years old, for example. Your advisor can help you determine how much you should buy based on the goal you have in mind and your monthly budget.

When talking about whole life insurance for adults, there are two standard ways advisors typically calculate how much life insurance coverage you should buy:

Option 1. The ‘ten times salary’ rule

Right now, your income is paying all or a portion of your household bills. If something happens to you, your family may have to make radical lifestyle changes that could include having to sell assets, downsize, or put off plans for post-secondary education.

Ideally, you would purchase the equivalent of at least 10 times your annual salary to give your family every advantage to carry on with confidence. If you can’t afford that much life insurance coverage right away, start with at least six times your annual income and adjust the coverage when you can.

Doing the math

- If you earn $75,000 a year after tax, you would need: $75,000 X 10 = $750,000.

- The minimum coverage you should consider is six times your annual salary: $75,000 X 6 = $450,000

Option 2. The ‘years to retirement’ rule

What if you have less than ten years between now and retirement? In this case, estimate the number of working years between now and retirement. That’s the income you need to replace with a life insurance policy.

This should be considered the minimum amount of coverage you need. There’s nothing stopping you from purchasing additional life insurance coverage, especially if you want to give your kids or grandchildren a financial leg up.

Doing the math

If you earn $75,000 after tax, multiply that amount by the number of years between now and retirement.

- 5 years to retirement: $75,000 x 5 = $375,000

- 8 years to retirement: $75,000 x 8 = $600,000

Whole Life Insurance through Serenia Life Financial

Whole life insurance is a valuable financial tool that provides lifelong coverage and the ability to grow your savings. It offers peace of mind knowing that your loved ones will be financially protected after your passing. By understanding how whole life insurance works in Canada, you can make an informed decision about which policy is right for you and your family.

If you’d like to learn more about whole life insurance, or if you would like to speak with a knowledgeable advisor at Serenia Life, fill out this form.

*Amounts calculated are based on total cash value, where the dividend option selected is paid-up additions.

{kind=link}

{kind=link}

{kind=link}

{kind=link}